Before CKYCRR, every bank, NBFC, Insurance company, mutual fund house, and securities intermediary maintained its own customer KYC repository. This results in

- The customer needs to submit KYC documents repeatedly.

- High operational costs and onboarding delays.

- Errors in customer information.

- High customer drop-off rates.

The CKYCRR resolves all these issues by keeping verified information. However, the system is only valuable if institutions use and maintain this repository carefully—not as a one-time process, but as an ongoing one.

“The need for a centralized KYC repository becomes even clearer when compared with the cost of traditional KYC operations. At the launch of the Central KYC Registry in 2016, DotEx International CEO Mukesh Agarwal stated that the platform could process uploads, downloads, and updates at an average cost of around ₹1 per transaction. By contrast, manual KYC verification often involves significantly higher operational costs due to document handling, verification, storage, and compliance reviews.”

What is CKYCRR?

CKYCRR a centralized record repository that stores and manages customer KYC records. It is managed by CERSAI. Whenever a financial institution onboards a customer, it must upload the verified KYC information to this repository.

After submission, the repository generates a unique 14-digit KIN, which is used to access the record, which helps in accessing the record.

Objective of CKYCRR: One Database for Every Reporting Entity.

In simple terms, CKYCRR works on a single principle: One Customer, One KYC Record. Instead of maintaining separate KYC files across multiple financial institutions, a single KYC record is stored. Any institution can access this record during customer onboarding instead of physical documentation.

Who Must Comply with CKYCRR?

CKYCRR compliance is mandatory for the following organizations:

| Regulator | Entities Covered |

| RBI | Commercial Banks, Payment Banks, Small Finance Banks, All NBFCs (Asset, Investment, Loan, Infrastructure), Cooperative Banks |

| SEBI | Stock Brokers, Depository Participants, Mutual Funds, Portfolio Managers, Research Analysts, Investment Advisers |

| IRDAI | All insurance companies (Life, General, Health), Insurance Intermediaries, Corporate Agents |

| PFRDA | National Pension System (NPS) Intermediaries, Pension Fund Managers |

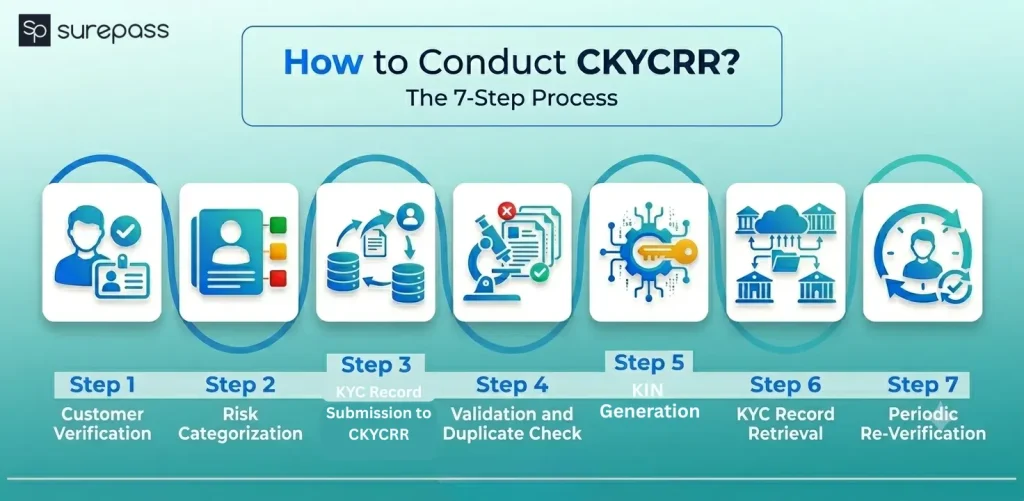

How to Conduct CKYCRR?

Here is the step-by-step process of how a financial institution uses CKYCRR:

Step 1: Customer Verification

When a customer completes KYC with a bank, NBFC, mutual fund, or insurance company, the organization collects and verifies their identity and address documents, such as:

- Aadhaar

- PAN

- Passport

- Voter ID

- Driving License

Step 2: Risk Categorization

After verification, the institution must categorise customer accounts according to their risk category.

- Low Risk

- Medium Risk

- High Risk

This classification helps financial institutions determine the frequency of future KYC record updates.

Automate your KYC Process & Reduce Fraud!

We have helped 3000+ companies in reducing Fraud by 95%

Step 3: KYC Record Submission to CKYCRR

The financial institution submits the verified customer record to CERSAI through the CKYCRR platform.

Step 4: Validation and Duplicate Check

Before creating a new record, CKYCRR verifies the submitted information and checks whether the customer already exists in the registry. The system compares details to prevent duplicate KYC records.

Step 5: KIN Generation

Once the record is verified, CKYCRR generates a unique 14-digit KYC identifier Number (KIN) or CKYC Number.

The KIN acts as a permanent reference number for the customer’s KYC record.

Step 6: KYC Record Retrieval

When the customer connects with another financial institution, the institution can search for the existing CKYC record using details such as:

- PAN

- Aadhaar

- Voter ID

- Driving License

After verifying the request and obtaining consent, the institution can retrieve the existing KYC record instead of collecting documents again. It reduces onboarding time and enhances customer experience.

Step 7: Periodic Re-Verification

Financial institutions must periodically review and update customer KYC records based on their risk category. High-risk customers require more frequent reverification than low-risk customers. Institutions should also update KYC records whenever there is a change in customer information, such as address, contact details, or identity proof.

What Details Are Submitted to CKYCRR?

After collecting and verifying the details, the following information must be uploaded to the registry:

| Required Information | Description |

| Demographic Details | Full Name, Date of Birth, Gender, Nationality |

| Contact Information | Mobile Number, Email Address, Permanent and Current Address |

| Identity Documents | Document Type (PAN, Aadhaar, Passport, Voter ID, Driving License, Document Number, Issuing Authority, Expiry Date) |

| Biometric/Photograph | Recent Customer Photograph (Passport Size) |

| Risk Classification | Low/Medium/High Risk Justification |

| FATCA/CRS Details | Tax residency and foreign account status |

| Beneficial Ownership | For legal entities |

Note for CKYC 2.0: The organization should submit data in JSON format with automated Aadhaar masking.

Risk-Based Re-Verification in CKYCRR

This centralized repository follows a risk-based approach:

| Risk Category | Re-Verification Frequency |

| High Risk | Every 2 Years |

| Medium Risk | Every 8 Years |

| Low Risk | Every 10 Years |

Institutions are required to periodically review customer records based on the assigned risk category and applicable regulatory guidelines.

CKYCRR 1.0 vs CKYCRR 2.0

The launch of CKYCRR 2.0 is announced in the Union Budget 2026, which will change the usual CKYCRR workflow completely.

| CKYCRR 1.0 | CKYCRR 2.0 | |

| Submission | Scheduled Batch File | Real Time API Call |

| Validation | Batch Report | Instant with API |

| De-duplication | Manual Review | AI-Assisted Matching |

| Data Masking | Manual | Automated |

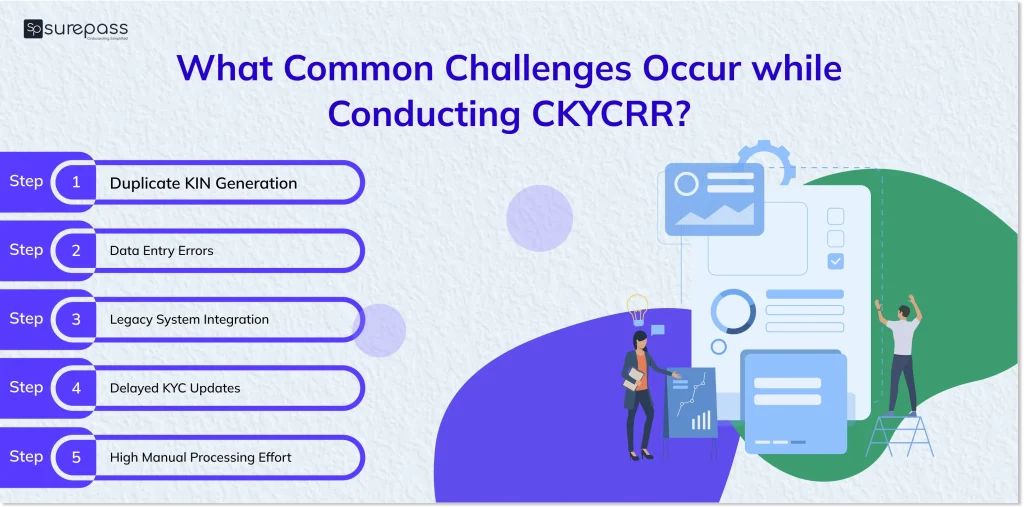

What Common Challenges Occur while Conducting CKYCRR?

Financial institutions face the following challenges in CKYCRR compliance:

- Duplicate KIN Generation: Minor differences in names, addresses, or identity documents can lead to duplicate records.

- Data Entry Errors: Incorrect customer information leads to validation failures or record mismatches.

- System Integration: Organizations using older onboarding systems may face integration challenges while adopting CKYC 2.0 workflows.

- Delayed Record Updates: Customer information must be updated in a timely manner to maintain accurate and compliant records.

How Can Surepass streamline the CKYCRR process with the Unified CKYC 2.0 Platform?

CKYC 2.0 introduces real-time validation, structured JSON submission, Aadhaar masking requirements, facial deduplication checks, and continuous lifecycle synchronization with CERSAI.

The Surepass CKYC 2.0 Platform simplifies the entire process with an automated and unified solution.

Organizations can search, download, upload, and update KYC records using a single platform. It automatically validates data against CKYC 2.0 requirements and guidelines to reduce rejection rates.

With this platform, organizations can submit records, track application status, and receive updates without having to rely on manual processes. With fully automated workflows, organizations can see a significant reduction in onboarding time and increase conversion.

FAQs

Ques: Is CKYCRR mandatory for all financial institutions?

Ans: Yes, CKYCRR compliance is mandatory for reporting entities regulated by RBI, SEBI, IRDAI, and PFRDA under the prevention of Money Laundering (Maintenance of Records) Rules, 2005. All the reporting entities must upload and maintain KYC records in the Central KYC Records Registry (CKYCRR).

Ques: Can a Customer have multiple KINs?

Ans: No, customers can have only one KIN (KYC Identifier Number). However, duplicate KINs can sometimes occur due to discrepancies in submitted information, such as name mismatches or document inconsistencies.

Ques: What documents are accepted for CKYCRR?

Ans: CKYCRR accepts all the OVDs (officially valid documents) such as Aadhaar, PAN, Passport, Driving License, Voter ID, and NREGA Job Card.

Ques: What is the difference between CKYCRR and CKYC?

Ans: CKYC (Central KYC) is a system that allows you to complete Know Your Customer verification once and use it across all financial institutions in India, such as banks, mutual funds, and insurance companies.

CKYCRR is the official body that operates the CKYC system. It receives, stores, and manages KYC records submitted by the financial institutions.

Ques: Can a financial institution access an existing CKYCRR record without the customer’s consent?

Ans: No, financial institutions cannot access or download existing CKYCRR records without explicit consent of the customer. The customer gets notified whenever their records are searched or retrieved.

Automate your KYC Process & Reduce Fraud!

We have helped 3000+ companies in reducing Fraud by 95%

")

")