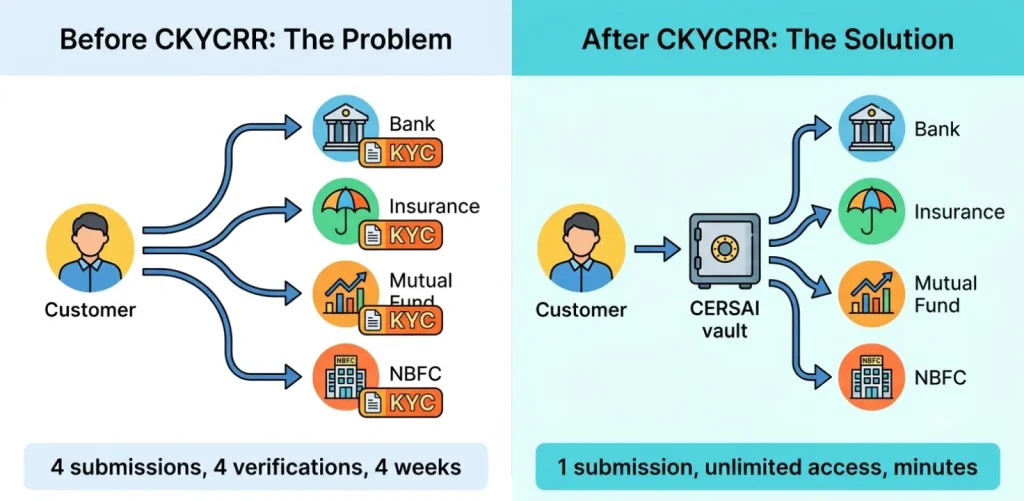

The repetitive KYC process with its lengthy paperwork and delayed onboarding ended when the Government of India, in collaboration with CERSAI, launched the CKYCRR (Central KYC Records Registry). This centralised repository stores verified KYC records accessible to all RBI, SEBI, IRDAI, and PFRDA-regulated institutions, eliminating duplicate submissions across the financial system.

With CKYCRR 2.0, customer onboarding has become much faster. Features like real-time validation, AI-powered face matching, and DigiLocker integration help complete the process in minutes instead of days. In this guide, we explain the CKYCRR full form, meaning, record-bearing reference, the 14-digit KIN, how to check your CKYC status online, what changed in CKYCRR 2.0, and how NRI customers are impacted.

What is CKYCRR Full Form?

CKYCRR stands for Central KYC Records Registry (also referred to as Central Know Your Customer Records Rules in the regulatory context). It is a centralised database managed by CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest of India) that stores and maintains verified KYC records of customers across India’s financial sector.

In simple terms, the CKYCRR meaning is a central system where your KYC data lives — so banks, insurance companies, mutual fund houses, and other SEBI/IRDAI/PFRDA-regulated entities can access it without asking you for the same documents again.

Automate your KYC Process & Reduce Fraud!

We have helped 3000+ companies in reducing Fraud by 95%

What is the CKYCRR Record?

A CKYCRR record is the digital file containing a customer’s verified Know Your Customer data. It includes identity proof, address proof, photograph, and signature stored in the central CERSAI registry. When a customer completes KYC at any financial institution, that institution uploads the verified data to CKYCRR. The record can then be retrieved by any other regulated entity with the customer’s consent.

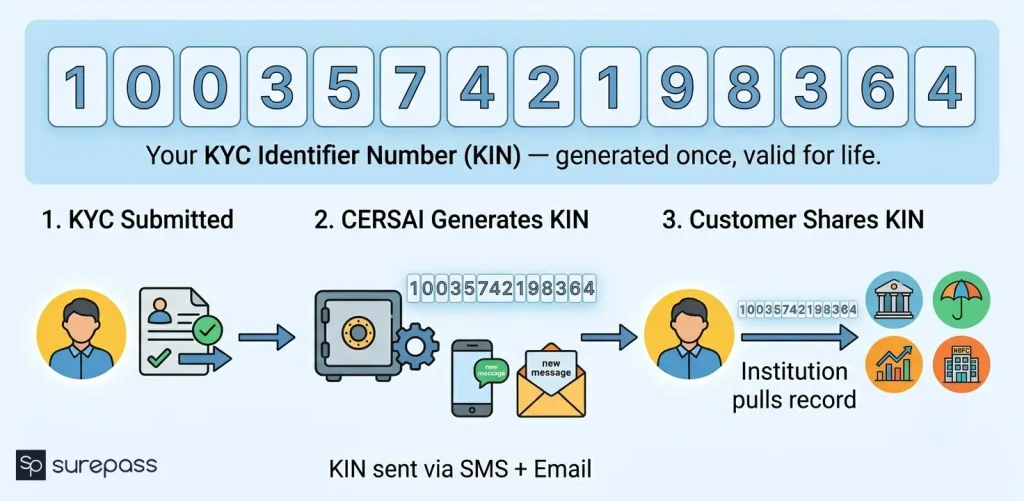

What is the CKYCRR Record Bearing Reference? (The 14-Digit KIN Explained)

The CKYCRR Record Bearing Reference is a unique 14-digit number officially called the KYC Identifier Number (KIN). It is generated by CERSAI after a customer’s KYC record is successfully uploaded for the first time.

Key facts about the KIN:

- It is a unique, permanent identifier assigned to each individual customer.

- It is sent to the customer via SMS and email on their registered contact details.

- Customers share this number with financial institutions instead of resubmitting physical documents.

- It allows any regulated entity to retrieve the full verified KYC record with customer OTP consent.

- It generally remains valid throughout the customer’s lifetime unless the record is modified, deactivated, or found to contain discrepancies.

Example: If you open a savings account at HDFC Bank and receive a KIN, you can share that same 14-digit number when opening a demat account with Zerodha or purchasing a life insurance policy without submitting the same KYC documents again.

Difference Between CKYC and CKYCRR

| Aspect | CKYC | CKYCRR |

| What it is | A process | A registry/database |

| Full form | Central Know Your Customer | Central KYC Records Registry |

| Function | The act of doing KYC once for multiple institutions | The system that stores and manages those records |

| Analogy | Filing a document | The filing cabinet where the document is kept |

| Governed by | RBI Master Direction on KYC | CERSAI under SARFAESI Act + PMLA |

What is the Purpose of CKYCRR?

CKYCRR was created to eliminate the inefficiency of India’s traditional KYC system, where customers had to submit the same documents to every financial institution they approached. The key purposes are:

- Eliminate repeated KYC document submission across different financial institutions.

- Reduce operational costs by giving institutions access to pre-verified records.

- Enhance data accuracy and security through a single, centralised record.

- Help regulators such as RBI, SEBI, IRDAI, and PFRDA monitor compliance more effectively.

- Create a uniform identity verification standard across all segments of India’s financial sector.

- Speed up customer onboarding from days to minutes for repeat customers.

Legal Framework: What Laws Govern CKYCRR?

CKYCRR operates within a regulatory framework supported by two major laws:

- Prevention of Money Laundering Act, 2002 (PMLA): Provides the AML foundation that makes KYC mandatory for all financial institutions. This act came into force in 2005.

- Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI): Section 20 authorised the creation of CERSAI as the central registry administrator.

Key regulatory notifications and rules:

- January 1, 2017: Ministry of Finance notification authorised CERSAI to function as the Central KYC Records Registry.

- December 18, 2020: RBI notification extended CKYCRR requirements to legal entities (companies, trusts) effective April 1, 2021.

- November 2024: RBI amendment aligned procedures with updated PMLA rules.

- June 2025: RBI circulars introduced extended timelines for low-risk customers and structured reminder systems.

Automate your KYC Process & Reduce Fraud!

We have helped 3000+ companies in reducing Fraud by 95%

CKYC Record Rules Every Financial Institution Must Know

- The 14-Digit KIN: Generated after first upload; the customer’s permanent KYC reference number.

- 10-Day Upload Window: Banks must upload a customer’s digital KYC within 10 days of account opening.

- 7-Day Update Rule: Any change in customer details (e.g., address) must be updated with CERSAI within 7 days.

- Consent is Mandatory: Customer OTP consent is required before retrieving their data from the registry.

- Document Quality: All scanned documents must be 150-200 DPI minimum to avoid rejection.

- Automatic Sync: When one institution updates a record, CERSAI notifies all other institutions where the customer is registered.

- Risk-Based Update Cycles: High-risk customers — re-verify every 2 years. Medium-risk — every 8 years. Low-risk — every 10 years.

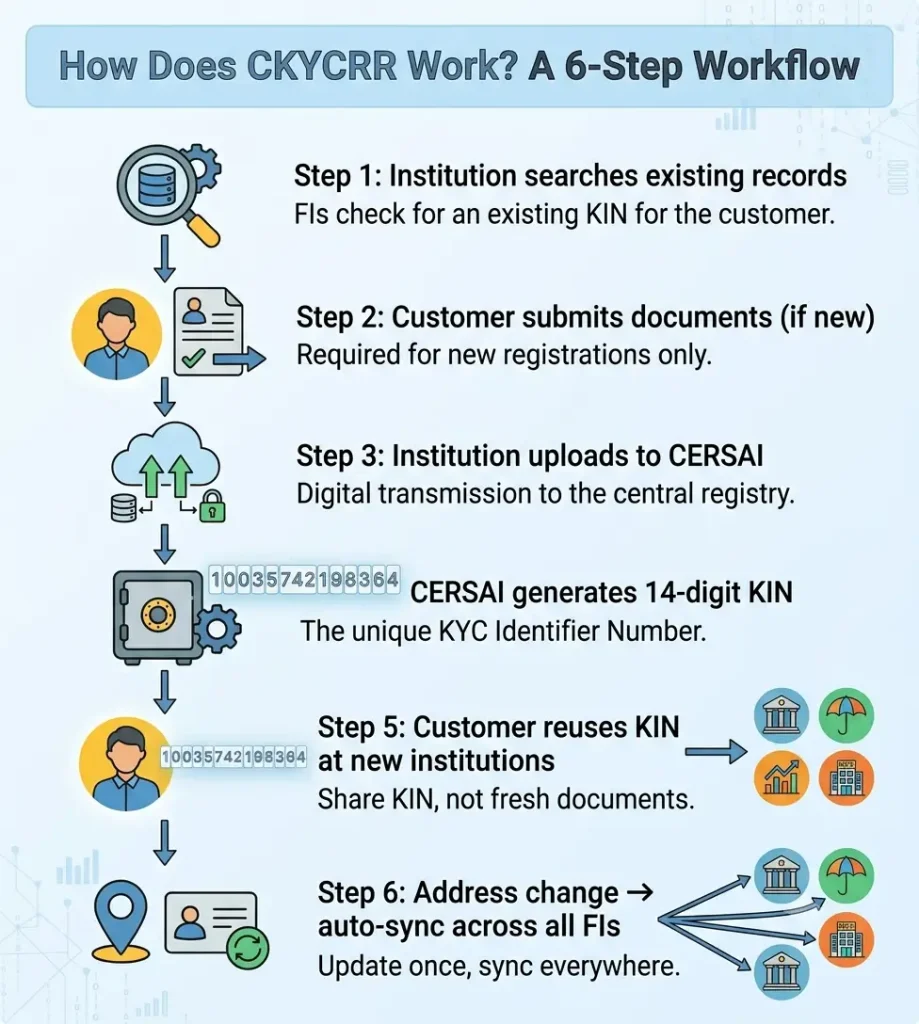

How Does CKYCRR Work? Step-by-Step

Step 1 — Search First

Before creating a new record, the financial institution searches the CKYCRR database using the customer’s PAN, Aadhaar number, or mobile number to check for an existing record. If found, it retrieves the record with customer OTP consent.

Step 2 — Document Submission (If No Existing Record Is Found)

The customer submits identity proof, address proof, and a recent passport-size photograph. After document verification, the institution digitises and validates the data.

Step 3 — Upload to CKYCRR

The verified data is uploaded to CERSAI’s registry — in real-time API format (CKYCRR 2.0) or via batch file (CKYCRR 1.0).

Step 4 — KIN Generated

CERSAI processes the record and generates the unique 14-digit KIN, which is sent to the customer by SMS and email.

Step 5 — Reuse Across Institutions

The customer shares the KIN with any future financial institution, which retrieves the record instantly without fresh documentation.

Step 6 — Lifecycle Updates

When a customer updates their details (e.g., new address), the updating institution pushes changes to CERSAI, which automatically notifies all linked institutions.

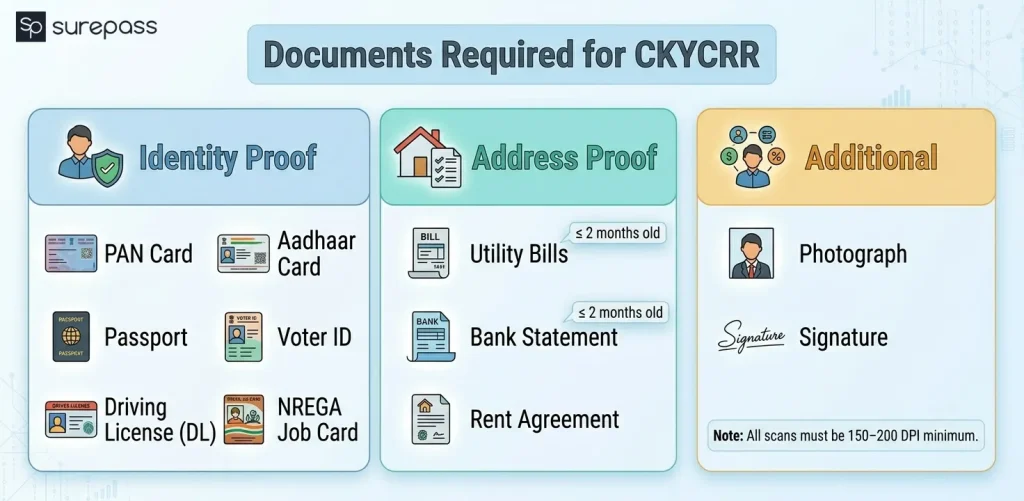

Documents Required for CKYCRR

The following documents are generally required when registering a CKYC record for the first time:

Proof of Identity (any one):

- PAN Card

- Aadhaar Card

- Passport

- Voter ID Card

- Driving Licence

- NREGA Job Card

Proof of Address (any one):

- Aadhaar Card

- Passport

- Voter ID Card

- Driving Licence

- Utility bills (electricity, water, telephone, gas — not older than 2 months)

- Bank account statement

- Rent agreement

Additional:

- Recent passport-size photograph

- Signature specimen

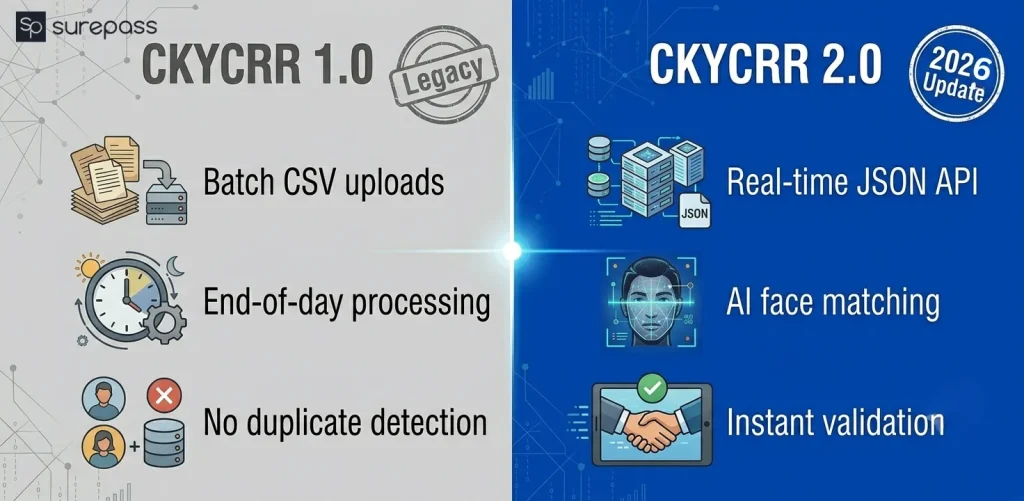

What is CKYCRR 2.0? Full Breakdown

CKYCRR 2.0 was announced in India’s Union Budget 2025 as a complete platform replacement not a simple upgrade. According to CERSAI’s April–June 2025 newsletter, the system now leverages AI-based matching algorithms and face match technology to significantly improve accuracy and efficiency in KYC verification.

Here is what changed from CKYCRR 1.0 to CKYCRR 2.0:

| Aspect | CKYCRR 1.0 | CKYCRR 2.0 |

| Submission Method | Bulk CSV/XML file uploads | Real-time REST API (JSON) |

| Validation Timing | Days after submission | Instant at the point of submission |

| Error Discovery | Delayed bulk rejection reports | Immediate field-level failure alerts |

| Document Quality | Lenient DPI standards | Strict DPI with auto-rejection |

| Aadhaar Privacy | Manual masking required | Automated mandatory masking |

| Duplicate Detection | ID-number matching only | AI facial recognition technology |

| Security Layer | Basic IP whitelisting | Mutual TLS (mTLS) authentication |

| Encryption | Simple XML protection | JWE with RSA-OAEP encryption |

| Customer Auth | Mobile OTP only | Multiple verification modes |

| Update Notifications | None from registry | Automatic push alerts to all FIs |

| Processing Speed | End-of-day batch processing | Continuous real-time processing |

| Legacy CBS Support | Native batch support | Requires a middleware/API layer |

The transition to CKYCRR 2.0 affects all 7,166+ reporting entities regulated by RBI, SEBI, IRDAI, and PFRDA. Institutions still running legacy Core Banking Systems (CBS) need a middleware integration layer to convert their data formats into the CERSAI 2.0-compliant JSON structure.

How to Check CKYCRR Status Online

You can verify whether you have an existing CKYCRR record through the following methods:

- Official Portal: Visit ckycindia.in and search using your PAN number. The system will display whether a record exists and the associated KIN.

- Through Your Bank: Ask your bank to perform a CKYCRR search using your PAN or Aadhaar number. If a record exists, they will retrieve it with your OTP consent.

- Via API (for institutions): Financial institutions can use CKYCRR Search APIs to check status programmatically in real time.

If your record is not found, it means either your first KYC was done before the 2017 digitisation mandate, or the institution has not yet uploaded your record to the registry.

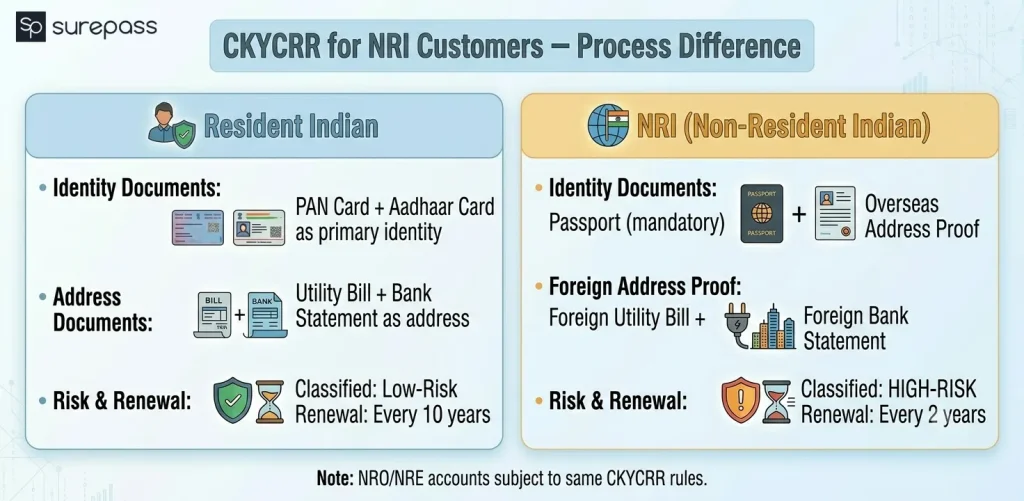

CKYCRR for NRI Customers

- Non-Resident Indian (NRI) customers can also be registered in the CKYCRR system, but with important differences:

- NRIs must provide Passport and Overseas Address Proof (foreign utility bill or bank statement from their country of residence).

- A PAN card is strongly recommended and may be mandatory for many financial products in India.

- NRI accounts are generally classified as high-risk for KYC purposes, requiring re-verification every 2 years.

- NRO (Non-Resident Ordinary) and NRE (Non-Resident External) accounts are subject to CKYCRR registration just like resident accounts.

- The KIN works the same way — once registered, NRI customers can reuse their record across all SEBI/IRDAI/PFRDA-regulated Indian institutions.

How to Access or Download Your CKYC Record

As a customer, you can access your CKYC record through:

Your Bank or NBFC: Request your institution to fetch your CKYCRR record. They will use your KIN and require OTP verification on your registered mobile number.

Official CKYC Portal: Visit ckycindia.in → Customer Section → enter PAN to retrieve your record details.

DigiLocker Integration (CKYCRR 2.0): Under CKYCRR 2.0, DigiLocker integration is expected to facilitate easier digital access and consent management for direct digital access and consent management by customers.

Benefits of CKYCRR for Customers and Financial Institutions

For Customers:

- Submit documents once; reuse across all financial institutions indefinitely.

- Faster account opening in minutes instead of days.

- NRI and migrant customers can open accounts in a new city without repeatedly submitting physical documents.

- Senior citizens and rural customers avoid repeated branch visits.

- More control over data through consent-based OTP access.

For Financial Institutions:

- Eliminate physical document storage and management costs.

- Detect fraud by cross-referencing customer data across institutions.

- Reduce KYC rejection rates with pre-validated, standardised records.

- Comply with RBI/SEBI/IRDAI audit requirements through CERSAI’s centralised audit trail.

- Better lending and risk decisions with a complete customer financial profile.

FAQs

Ques: What is the full form of CKYCRR?

Ans: CKYCRR stands for Central KYC Records Registry (or Central Know Your Customer Records Rules in the regulatory framework). It is managed by CERSAI under RBI oversight.

Ques: Is CKYCRR mandatory?

Ans: Yes. CKYCRR compliance is mandatory for all institutions regulated by RBI, SEBI, IRDAI, and PFRDA. Individual accounts must be registered from January 1, 2017 onward; legal entities from April 1, 2021.

Ques: What is the CKYCRR KIN number?

Ans: KIN is a unique 14-digit KYC Identifier Number generated by CERSAI when your record is first created. It can be used to share your verified KYC details with any regulated financial institution.

Ques: How do I check my CKYCRR status?

Ans: Visit ckycindia.in and search with your PAN number, or ask your bank to search on your behalf using your PAN or Aadhaar with your OTP consent.

Ques: What changed in CKYCRR 2.0?

Ans: CKYCRR 2.0 replaced batch CSV uploads with real-time JSON APIs, added AI facial de-duplication, made Aadhaar masking mandatory, strengthened encryption (JWE/RSA-OAEP), and introduced automatic update notifications to all linked institutions.

Ques: What documents are required for CKYCRR?

Ans: You need one proof of identity (PAN, Aadhaar, passport, Voter ID, or driving licence), one proof of address (Aadhaar, utility bill under 2 months old, bank statement), a recent photograph, and signature specimen.

Ques: Can NRI customers register for CKYCRR?

Ans: Yes. NRI customers can register using their passport as identity proof and a foreign address document. NRI accounts are classified as high-risk and require re-verification every 2 years.

Automate your KYC Process & Reduce Fraud!

We have helped 3000+ companies in reducing Fraud by 95%

")

")