In the financial sector, CRILC plays an important role in providing high-stress borrowers’ data. Banks and financial institutions use CRILC to check borrowers’ financial health, repayment performance, and credit risk. It will help in the early detection of potential stress or default risks. This system helps in informed decision-making, better credit management, reduced non-performing assets, and financial stability. To get more information about this repository read the blog thoroughly.

What is CRILC?

CRILC full form is the Central Repository of Information on Large Credits. It collects, stores, and disseminates information about borrowers with large exposure. The RBI (Reserve Bank of India) maintains this database. This database helps financial institutions monitor the credit exposure of borrowers. It helps detect the potential risk of defaults.

Features of CRILC

Purpose: It aims to strengthen the credit risk management framework with early detection of stressed assets in the banking system.

Coverage: It covers all borrowers with aggregator fund-based and non-fund-based exposure of ₹5 crores and above.

Reporting Entities: Scheduled commercial banks, cooperative banks, non-banking financial companies (NBFCs), and all India Financial Institutions are required to report to CRILC.

Data Collection: It collects SMAs (Special Mentioned Accounts), large credit exposure, and borrower data. It stores account balances, credit limits, and repayment performance data.

Monitoring: RBI monitors the borrower status and repayment history by using CRILC data. It makes sure that financial institutions maintain credit discipline. This will help in reducing NPAs.

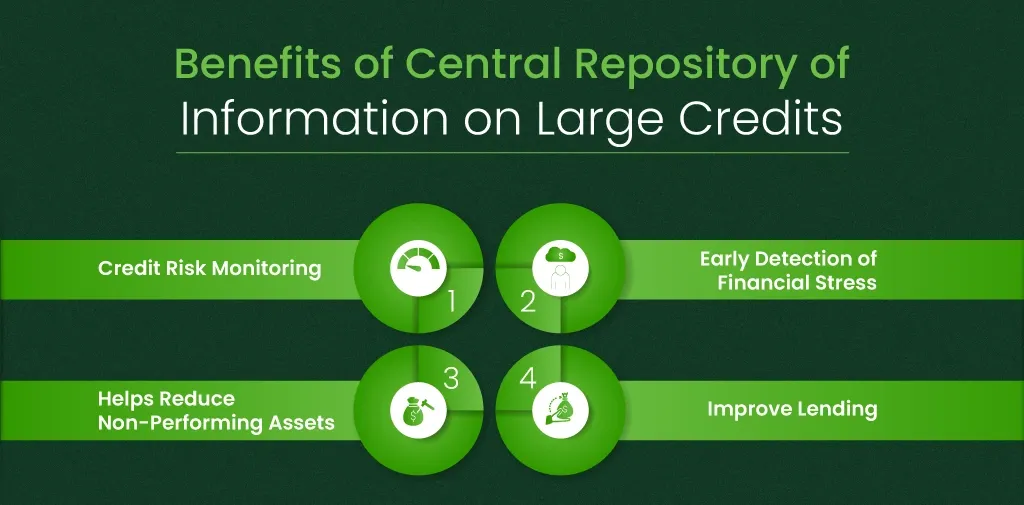

Benefits of Central Repository of Information on Large Credits

These are the following benefits of the Central Repository of Information on Large Credits:

- Credit Risk Monitoring: Financial Institutions and banks can use CRILC to evaluate credit risk and improve asset quality. This proper evaluation will minimize losses from the bad loans.

- Early Detection of Financial Stress: It helps find borrowers under financial stress or at risk of default by checking Special Mention Accounts (SMAs). Banks can flag the accounts and prevent financial losses with proper management of potential defaults.

- Helps Reduce Non-Performing Assets: It allows tracking and management of large borrowers’ repayment behaviors. This repository helps financial institutions identify the repayment delays early. This will help them take the right actions and provide support to borrowers. With proper measures and action, they can reduce the risk of NPAs (Non-Performing Assets).

- Improve Lending: Banks and financial institutions use CRILC data to evaluate the financial health of Borrowers. By checking borrowers’ credit history, repayment habits, and exposure levels, lenders can set appropriate loan terms. It will reduce the risk of defaults and lending to high-risk borrowers.

Automate your KYC Process & reduce Fraud!

We have helped 200+ companies in reducing Fraud by 95%

What is the CRILC Report?

It is a report that provides information about a borrower’s credit exposure. It helps in tracking the large credit exposure borrowers. Banks and financial institutions must report about the borrowers with aggregator credit exposures of rupees 5 crores and above.

Important Things to Know About the CRILC Report

Information

The report contains the following information:

- Borrower Details

- Credit Facility Type (e.g., term loan, working capital loans).

- Exposure Amounts.

- Classification Status (e.g., Special Mention Accounts or SMA).

Frequency of Crilc Reporting

It is a must for financial institutions and banks to submit reports quarterly. Significant changes in borrower accounts, need to be updated frequently.

Key Terms in Central Repository of Information on Large Credits

- RFA in CRILC: RFA refers to the Risk Framework Approach. It helps check the risk of providing loans to borrowers with an evaluation of financial behavior, credit history, and potential for repayment.

- SMA in CRILC: SMA stands for Special Mention Account. Banks use this classification to classify borrowers who show signs of potential financial stress without default. The SMA is divided into three sections.

- SMA-0: Accounts where the payment is overdue for 1-30 days.

- SMA-1: Account where the payment is overdue for 31-60 days.

- SMA-2: Accounts where payment is overdue for 61-90 days.

Challenges and Limitations of Reporting

These are the following challenges banks and financial institutions face that sometimes result in penalties.

Reporting Delays: Sometimes, Financial institutions are unable to report on time (due to some reasons). It impacts the timely detection of risks.

Data Accuracy: Incorrect or incomplete data submission can lead to misinterpretations and wrong decisions.

Conclusion

Crilc (Central Repository of Information on Large Credits) is a centralized database. It collects, stores, and shares borrowers’ information. It helps in the early detection of financial stress, informed decision-making in lending, and reduced NPAs. It focuses on monitoring large credit exposures and SMAs. This will ensure that financial institutions can manage risk effectively.

FAQs

Ques: What is CRILC?

Ans: Central Repository of Information on Large Credits is a database that stores, and shares information about borrower credit exposure.

Ques: Which accounts are reported in CRILC?

Ans: Accounts with credit exposure of rupees 5 crore and above, including term loans, working capital, and credit facilities, are reported in CRILC.

Ques: What is the frequency of CRILC reporting?

Ans: Frequency of CRILC reporting is done quarterly by banks and financial institutions.

Ques: What is the purpose of the CRILC?

Ans: The purpose of the Central Repository of Information on Large Credits is to monitor and manage credit risk by tracking the credit exposure of borrowers to financial institutions.

Ques: What is the threshold limit for Crilc?

Ans: The threshold limit is Rupees 5 crore.

Ques: What is RFA in CRILC?

Ans: RFA refers to a red flag account.

Ques: What is CRILC RBI?

Ans: It is a centralized database maintained by the RBI.

Ques: What is the Full Form of SMA in CRILC?

Ans: SMA full form in Special Mention Account.

Ques: Do NBFCs report in CRILC?

Ans: Yes, it is a must for NBFCs to report credit information to CRILC.

Ques: What is CRILC’s full form in Banking?

Ans: Its full form is the Central Repository of Information on Large Credits.

Automate your KYC Process & reduce Fraud!

We have helped 200+ companies in reducing Fraud by 95%

")

_ Full Comparison")