Crypto

Fraud Prevention for Crypto

With over 420 million crypto users worldwide, stopping fraud is more important than ever. As the crypto space grows, so do scams, hacks, and other threats. Using smart technologies like machine learning, crypto platforms can spot suspicious behavior early, block fraud, and keep users safe—without slowing things down. Don’t rely on outdated methods. Stay secure, stay compliant, and stop fraud before it happens.

Trusted by over 3,000+ companies of all sizes

What are the most common types of crypto fraud?

How can I identify a phishing attempt?

Is it safe to share my wallet seed phrase or private key?

How can I verify if a crypto project or exchange is legitimate?

What should I do if I suspect I’ve been scammed?

How can I secure my crypto wallet?

What are red flags in crypto investment offers?

Does using a centralized exchange protect me from fraud?

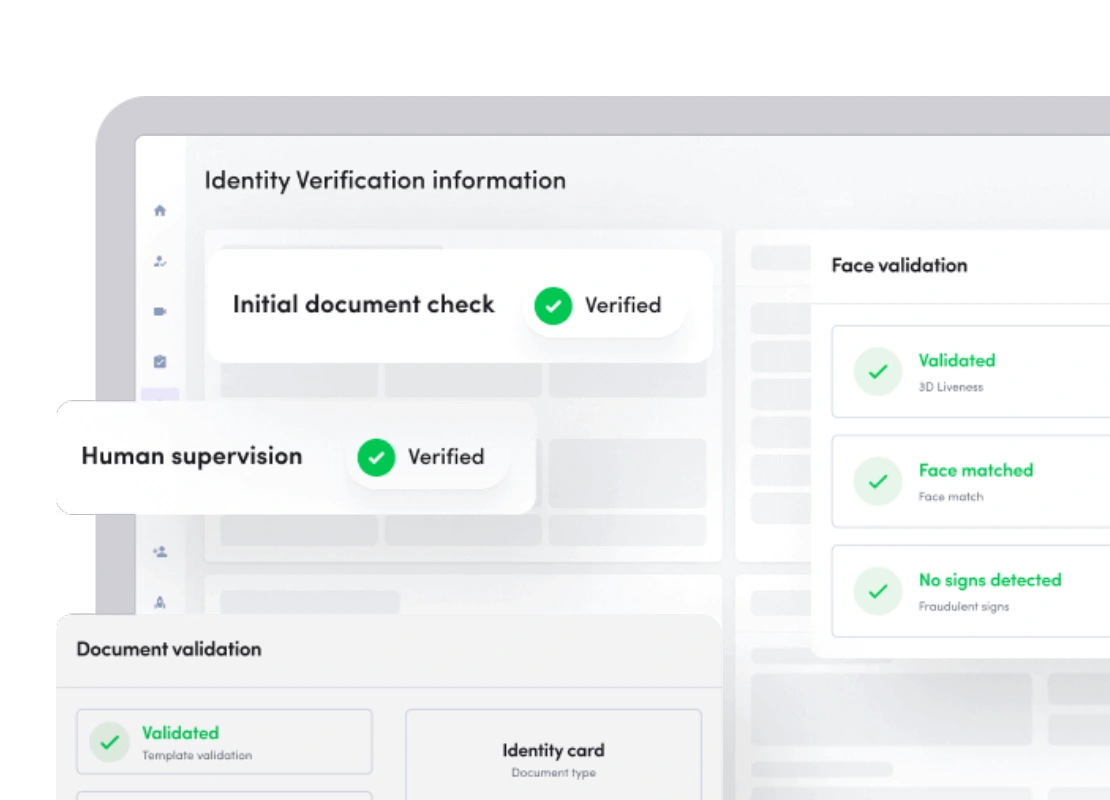

Ready to Supercharge Your Business?

Boost growth, security, and efficiency with Surepass’s advanced verification solutions.

Get API Key

By creating a free account, you get

Gain access to over 300+ verification APIs to streamline your KYC/KYB processes effortlessly.

Test our APIs in a secure sandbox environment to ensure smooth functionality and integration.

Enjoy seamless integration with developer-friendly documentation and 24/7 expert support.

Trusted by over 3,000+ companies of all sizes

Build with us

We’d love to show you how Surepass can help your business. Fill out the form and we’ll be in touch within 24 hours

For all updates & much more, mail on [email protected]

We respect your privacy.